Summary

AI automation has a great impact on the insurance industry. This technology reduces operational costs, improves efficiency, and enhances decision-making. This guide highlights how insurers can leverage automation across underwriting, claims, fraud detection, and customer service while maximizing ROI through strategic implementation, advanced technologies, and data-driven workflows designed for scalable and sustainable growth.

Quick Overview

- AI automation reduces operational costs across core insurance business functions.

- Intelligent systems improve underwriting accuracy and claims processing timelines.

- Automation enhances customer experience and offers faster service interactions.

- Fraud detection becomes more efficient with real-time data analysis capabilities.

- Strategic implementation provides measurable ROI and long-term business scalability.

The AI insurance market, valued at $8.63 billion in 2025, is rapidly scaling with over 25% projected spending growth in 2026. It signals a fundamental change in how insurers operate, compete, and grow. The real question is not whether AI will transform insurance, but how quickly businesses can adapt to stay ahead.

If you have ever felt the pressure of rising operational costs, slower claims processing, or increasing customer expectations, you are not alone. Insurance companies today are expected to do more with less, deliver faster services, reduce risks, and improve accuracy, all while maintaining profitability. That’s exactly where AI automation in insurance starts to make a measurable difference.

AI in insurance reduces manual underwriting time, detects fraud before it impacts your bottom line, and resolves claims in hours instead of days. It unlocks smarter decision-making and creates a system that continuously improves itself. And the best part? You don’t need to overhaul everything to start seeing results.

In this guide, we’ll break down how AI automation in insurance directly reduces costs and boosts ROI, with practical insights you can actually implement. Whether you are exploring artificial intelligence solutions for the first time or looking to scale existing systems, you’ll discover where the real value lies.

What Is AI Automation in Insurance?

AI automation in insurance refers to the use of artificial intelligence technologies to handle repetitive, data-driven, and decision-based tasks across insurance operations with minimal human intervention. Instead of relying on manual processes, insurers use AI to analyze data, make predictions, and execute workflows faster and more accurately.

At its core, AI automation combines technologies such as machine learning, natural language processing, insurance LLMs, and predictive advanced analytics to streamline key functions, including underwriting, claims processing, customer support, and fraud detection. For example, an AI for insurance claims systems can automatically review documents, validate policy details, detect anomalies, and even approve simple claims in real time.

Similarly, AI for insurance underwriting models can assess risk profiles by analyzing historical data, customer behavior, and external factors, helping insurers make more informed decisions. In simple terms, AI automation is like having a super-smart helper who learns from experience and handles your repetitive work quickly every time.

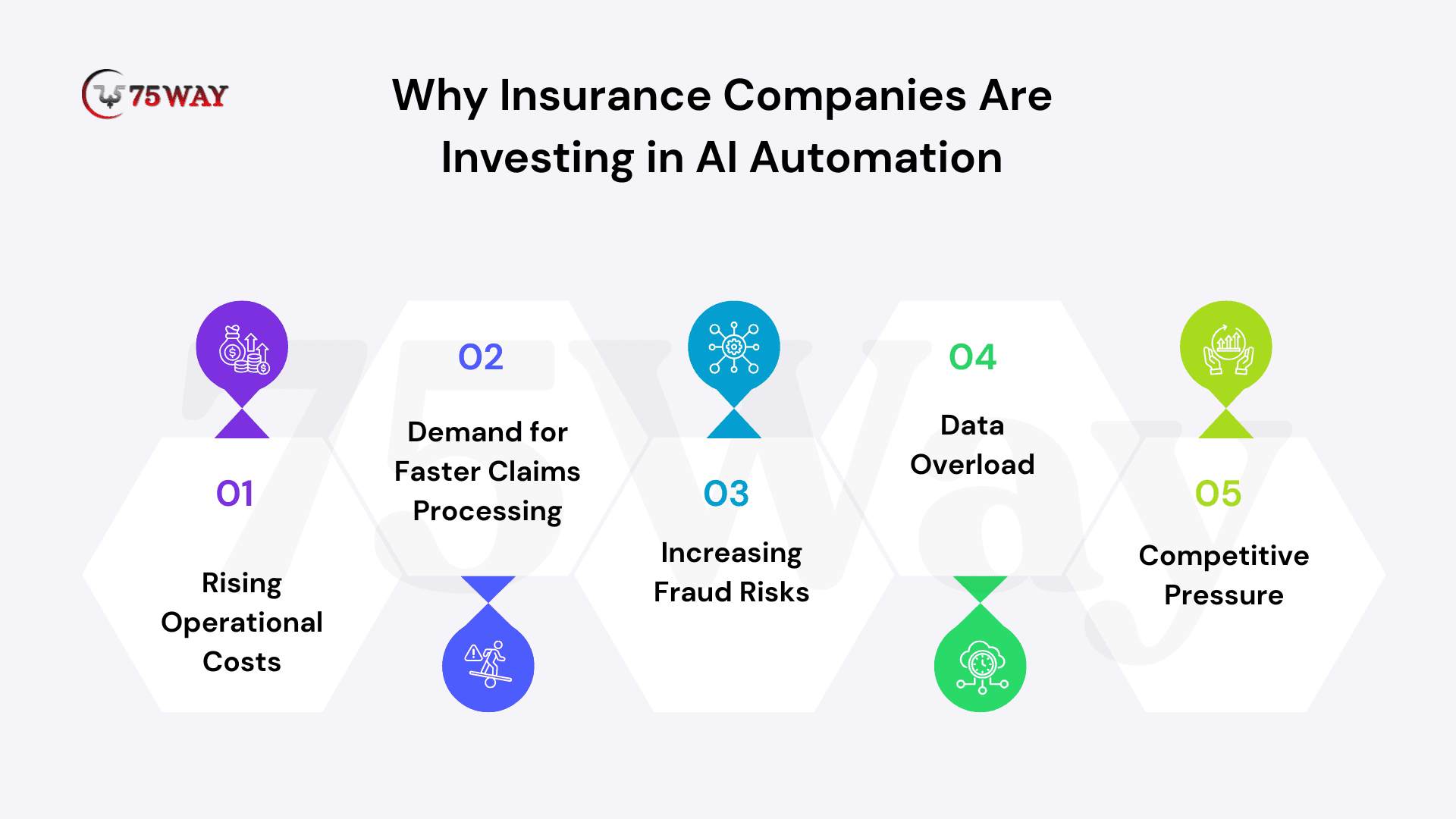

Why Insurance Companies Are Investing in AI Automation?

- Rising Operational Costs: Manual processes increase overhead and slow down productivity. Automation reduces dependency on repetitive human tasks.

- Demand for Faster Claims Processing: Customers expect quick resolutions. Delays directly impact satisfaction and retention.

- Increasing Fraud Risks: Fraudulent claims are becoming more sophisticated. AI systems help detect anomalies in real time.

- Data Overload: Insurers handle vast amounts of data daily. AI helps extract actionable insights efficiently.

- Competitive Pressure: Organizations adopting automation gain a clear advantage in speed, cost, and customer experience.

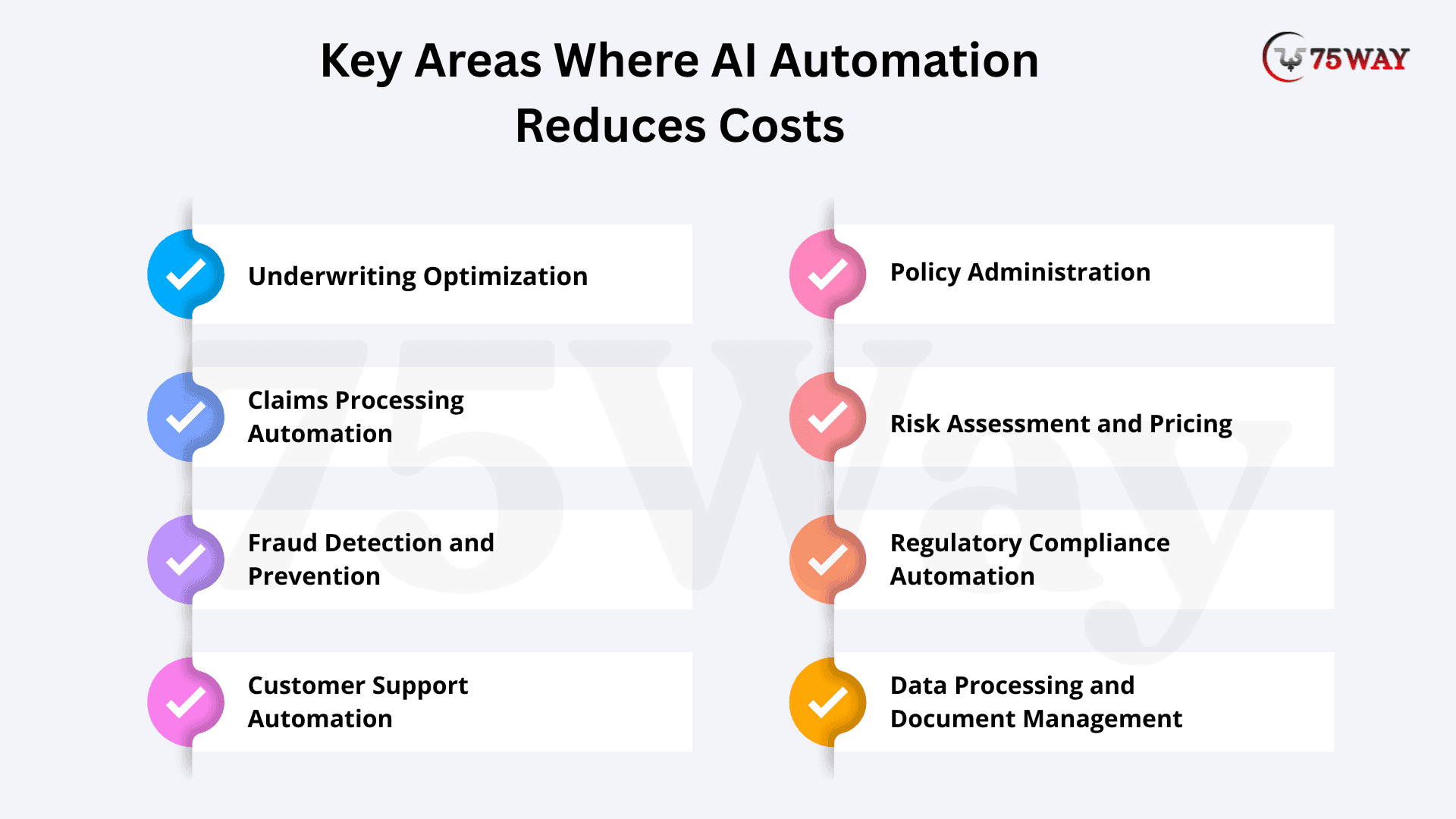

Key Areas Where AI Automation for Insurance Reduces Costs

AI automation delivers cost savings by transforming core insurance functions into faster, data-driven, and highly efficient systems. From underwriting to customer support, it minimizes manual effort, reduces errors, and accelerates decision-making. The result is lower operational expenses, improved accuracy, and scalable processes that directly contribute to stronger profitability and higher ROI.

- Underwriting Optimization

AI for insurance underwriting analyzes historical data, risk profiles, and external factors to assess applications faster and more accurately. This reduces manual effort and minimizes errors, leading to better risk selection and cost savings. It enables insurers to process higher volumes without increasing staff. Decisions become more consistent and data-driven.

- Claims Processing Automation

Automation accelerates claim verification, document analysis, and settlement decisions. This reduces processing time and administrative costs. Faster processing improves customer satisfaction and retention. It also minimizes human errors during claim evaluations. Insurers can handle large claim volumes efficiently during peak periods.

- Fraud Detection and Prevention

AI models identify suspicious patterns and flag potential fraud before payouts are made. This prevents financial losses and improves overall efficiency. Early detection reduces investigation costs and unnecessary payouts. AI-powered document fraud detection systems continuously learn from new patterns of fraud. This strengthens long-term risk management strategies.

- Customer Support Automation

Conversational AI in insurance handles queries, policy updates, and support requests, reducing the need for large support teams. This ensures faster response times and consistent customer experiences. AI voice agents for insurance operate around the clock without increasing operational costs. Support teams can focus on complex issues. Overall service quality improves while costs decrease.

- Policy Administration

Automating policy issuance, renewals, and updates reduces manual workload and improves operational efficiency. This minimizes processing delays and administrative errors. It ensures accurate record management across systems. Staff productivity increases with reduced repetitive tasks. Overall operational costs decline while scalability improves.

- Risk Assessment and Pricing

AI-driven models evaluate real-time data, customer behavior, and market trends to optimize pricing strategies. AI for risk management improves accuracy in premium calculations and reduces underpricing risks. Dynamic pricing enhances competitiveness in the market. It also ensures better alignment with actual risk exposure. Profit margins improve through smarter pricing decisions.

- Regulatory Compliance Automation

AI systems monitor regulations and automatically ensure processes align with compliance requirements. This reduces the risk of penalties and manual compliance checks. It simplifies audit preparation and reporting processes. Continuous monitoring minimizes human oversight errors. Overall, compliance management becomes faster, more reliable, and cost-efficient.

- Data Processing and Document Management

AI automates the extraction, classification, and processing of large volumes of documents and data. This reduces dependency on manual data entry tasks. It improves accuracy and speeds up information retrieval. Operational bottlenecks caused by paperwork are eliminated. Teams can focus on higher-value strategic activities.

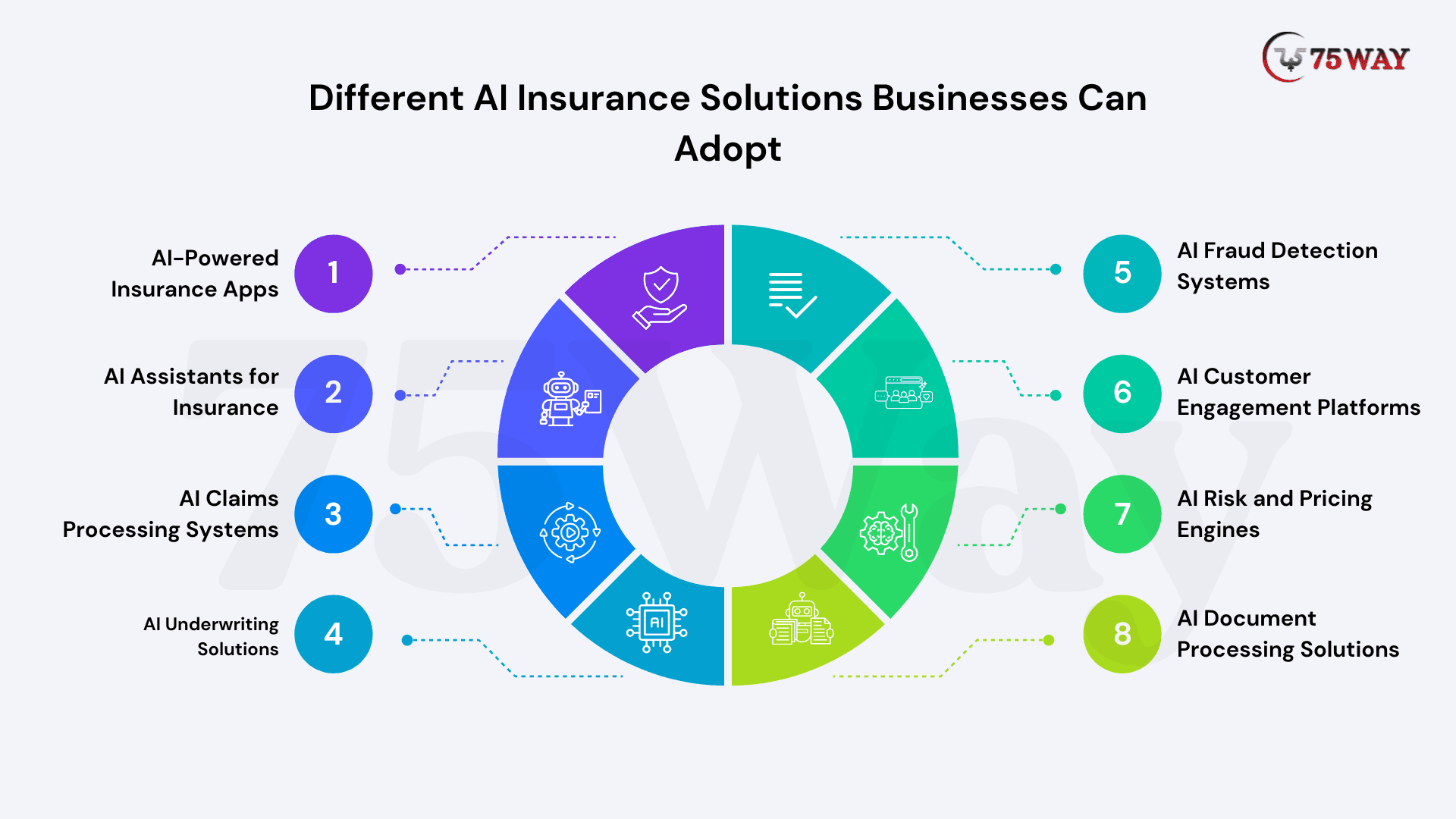

Different AI Insurance Solutions Businesses Can Adopt

AI insurance solutions help businesses automate core operations, reduce manual workload, improve accuracy, and enhance customer experience. They also significantly lower operational costs while boosting overall profitability.

- AI-Powered Insurance Apps

AI-powered insurance apps allow customers to manage policies, file claims, and receive support directly from their mobile devices. These mobile app development solutions use intelligent algorithms to personalize user experiences and recommendations. They reduce dependency on manual processes while improving engagement, accessibility, and overall customer satisfaction.

- AI Assistants for Insurance

AI assistants handle customer queries, guide users through policy details, and assist with claims or renewals in real time. These autonomous AI agents use natural language understanding to deliver accurate responses instantly. This reduces support workload while ensuring faster service, improved customer experience, and round-the-clock availability without additional staffing costs.

- AI Claims Processing Systems

AI claims systems automate document verification, damage assessment, and settlement decisions with minimal human involvement. They analyze images, forms, and historical data to speed up approvals. AI for insurance claims reduces processing time, lowers operational costs, and improves accuracy while enabling insurers to handle high claim volumes efficiently.

- AI Underwriting Solutions

AI underwriting solutions assess risk profiles using historical data, behavioral insights, and external data sources quickly. They help insurers make smarter policy decisions without relying on manual evaluations. This improves risk selection, reduces errors, and enhances scalability while maintaining consistent and data-driven underwriting processes.

- AI Fraud Detection Systems

AI fraud detection systems identify suspicious patterns and anomalies in claims and transactions before payouts are made. They continuously learn from new data to improve detection accuracy over time. This helps insurers prevent financial losses, reduce investigation costs, and strengthen overall fraud prevention strategies effectively.

- AI Customer Engagement Platforms

AI engagement platforms personalize communication across emails, apps, and chat interfaces based on customer behavior and preferences. They help insurers deliver targeted offers and timely updates. This increases customer retention, improves satisfaction, and drives higher conversion rates without requiring large marketing or support teams.

- AI Risk and Pricing Engines

AI risk and pricing engines analyze real-time data, market trends, and customer profiles to determine optimal premium pricing strategies. They adjust pricing dynamically to reflect actual risk levels. This improves competitiveness, reduces underpricing risks, and helps insurers maximize profitability through more accurate and responsive pricing decisions.

- AI Document Processing Solutions

AI document processing solutions extract, classify, and organize data from large volumes of structured and unstructured documents automatically. They eliminate manual data entry and reduce processing errors. This speeds up operations, improves data accuracy, and allows teams to focus on higher-value tasks instead of repetitive paperwork.

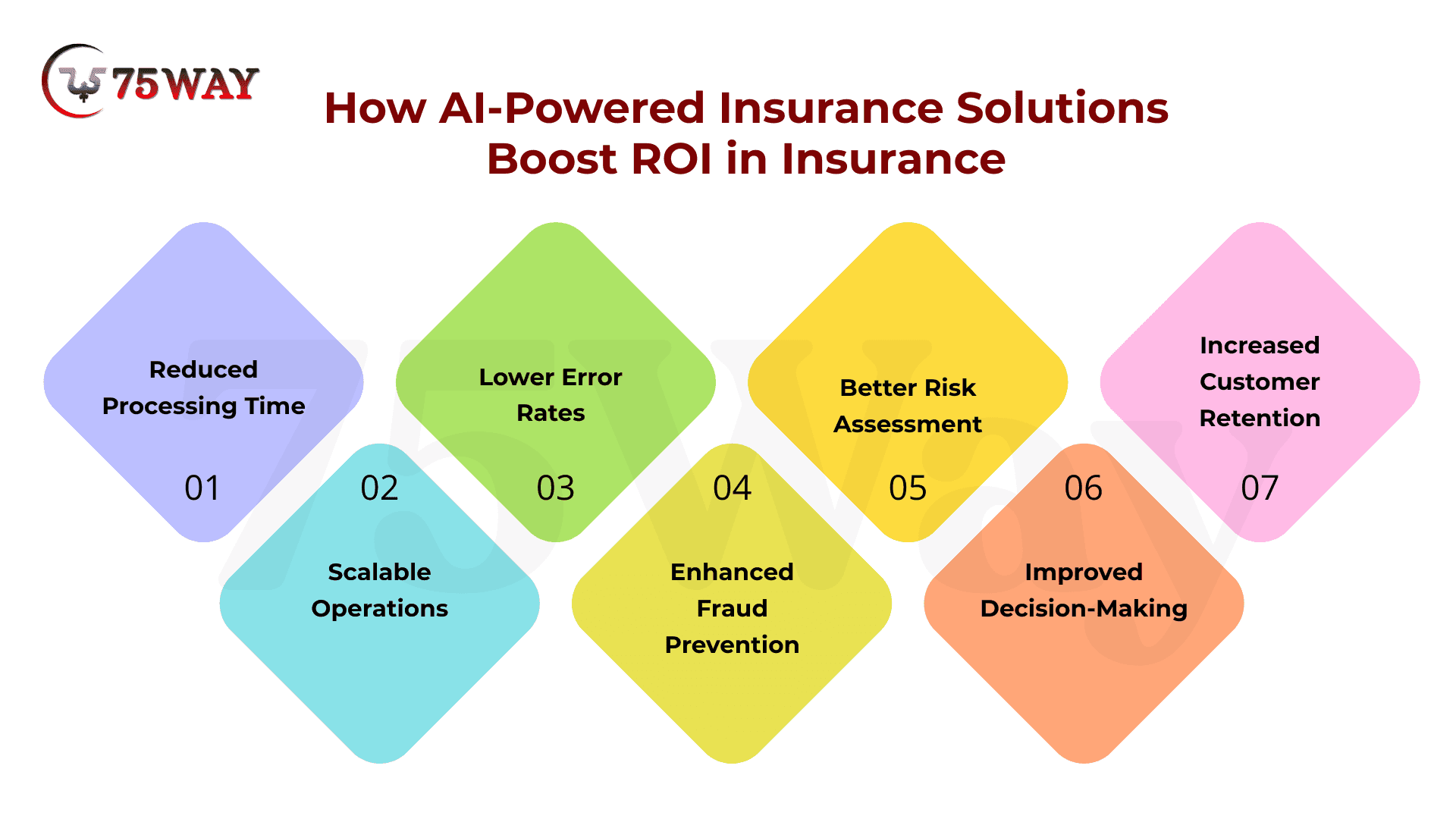

How AI-Powered Insurance Solutions Boost ROI in Insurance?

AI automation boosts ROI in insurance by improving efficiency across every stage of operations. It reduces processing time, minimizes costly errors, enhances risk assessment accuracy, and strengthens customer relationships. These improvements allow insurers to scale faster, operate more efficiently, and generate higher profitability without significantly increasing operational expenses.

- Reduced Processing Time: Faster operations increase throughput without adding workforce, enabling insurers to process claims and underwriting faster.

- Lower Error Rates: AI in insurance reduces human errors in data entry and processing, minimizing rework, disputes, and unnecessary operational correction costs.

- Better Risk Assessment: AI improves underwriting accuracy by analyzing large datasets, helping insurers price policies correctly and avoid high-risk losses.

- Increased Customer Retention: Faster, personalized services improve customer satisfaction and loyalty, reducing churn and lowering acquisition costs over time.

- Scalable Operations: Automation allows insurers to handle growing workloads efficiently without proportional increases in staff or operational expenses.

- Enhanced Fraud Prevention: AI detects suspicious patterns early, preventing fraudulent claims and reducing financial losses before payouts are made.

- Improved Decision-Making: AI insurance solutions deliver real-time insights from data, enabling faster, smarter, and more accurate business and risk decisions.

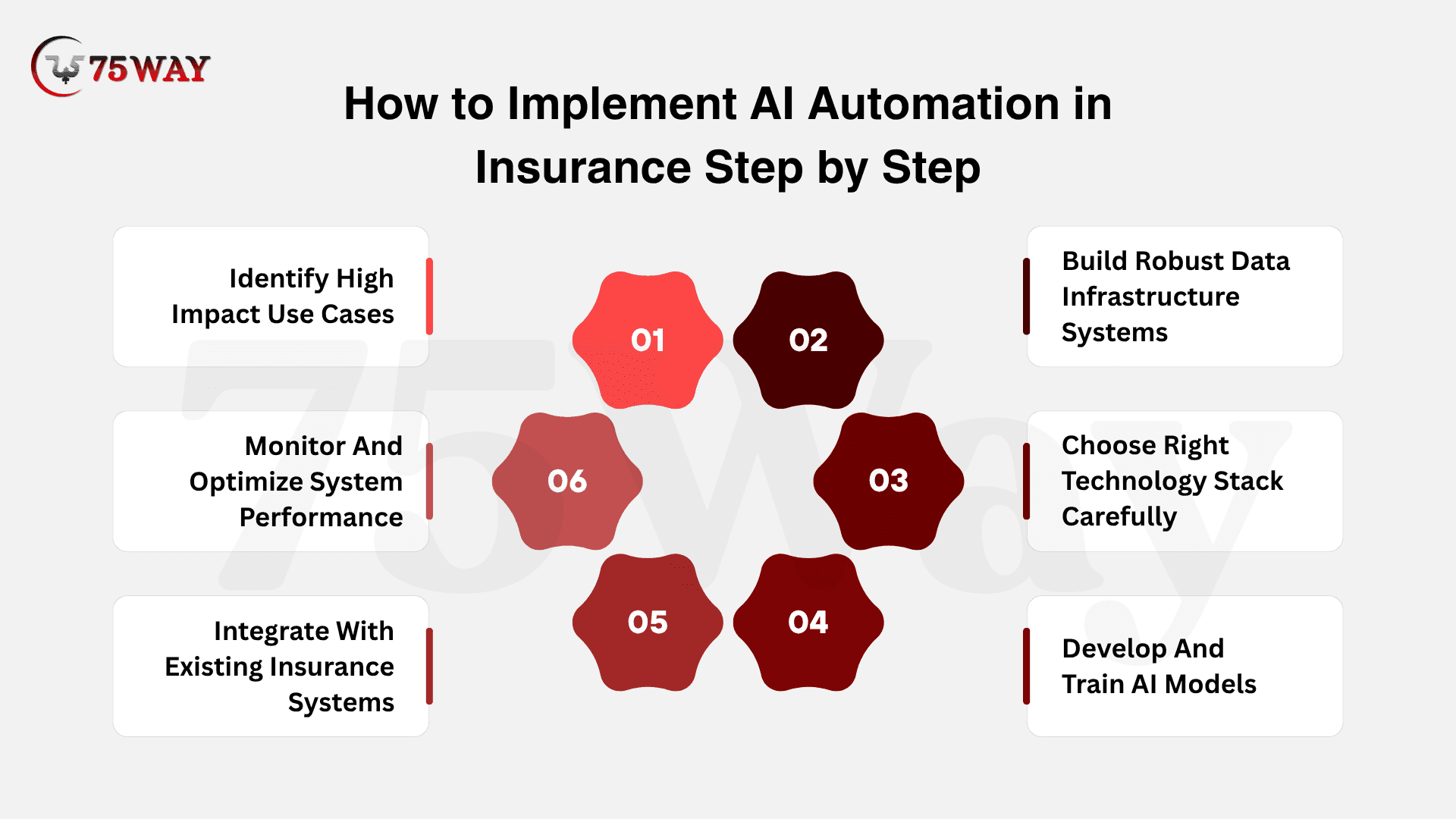

How to Implement AI Automation in Insurance Step by Step?

Implementing AI automation in insurance requires a structured approach that focuses on identifying the right opportunities, preparing strong data systems, and ensuring smooth integration with existing operations. A well-planned execution helps insurers reduce risks, control costs, and maximize long-term ROI.

- Identify High Impact Use Cases

Start by pinpointing processes that cause delays, high costs, or frequent errors. Areas like claims processing, underwriting, fraud detection, and customer support often deliver the fastest and most measurable impact when automated effectively.

- Build Robust Data Infrastructure Systems

Strong AI systems depend on clean, organized, and secure data. Insurers must consolidate information from multiple sources, remove inconsistencies, and ensure real-time accessibility so AI models can generate accurate insights and reliable outcomes.

- Choose The Right Technology Stack

Selecting the right combination of AI tools, platforms, and frameworks ensures scalability and smooth deployment. The focus should be on compatibility with existing systems, long-term support, and the ability to handle growing data and workload demands.

- Develop And Train AI Models

AI models must be trained using relevant insurance datasets to reflect real-world scenarios. Continuous refinement improves accuracy in predictions, risk assessment, and decision-making, making automation more reliable over time.

- Integrate With Existing Insurance Systems

Seamless integration with legacy insurance systems is essential to avoid disruption. Proper connectivity ensures smooth data flow between departments, enabling end-to-end automation without breaking existing operational processes.

- Monitor And Optimize System Performance

Ongoing monitoring helps track efficiency, accuracy, and cost savings. Regular performance checks allow insurers to fine-tune AI systems, fix gaps, and ensure consistent improvement in results and operational outcomes.

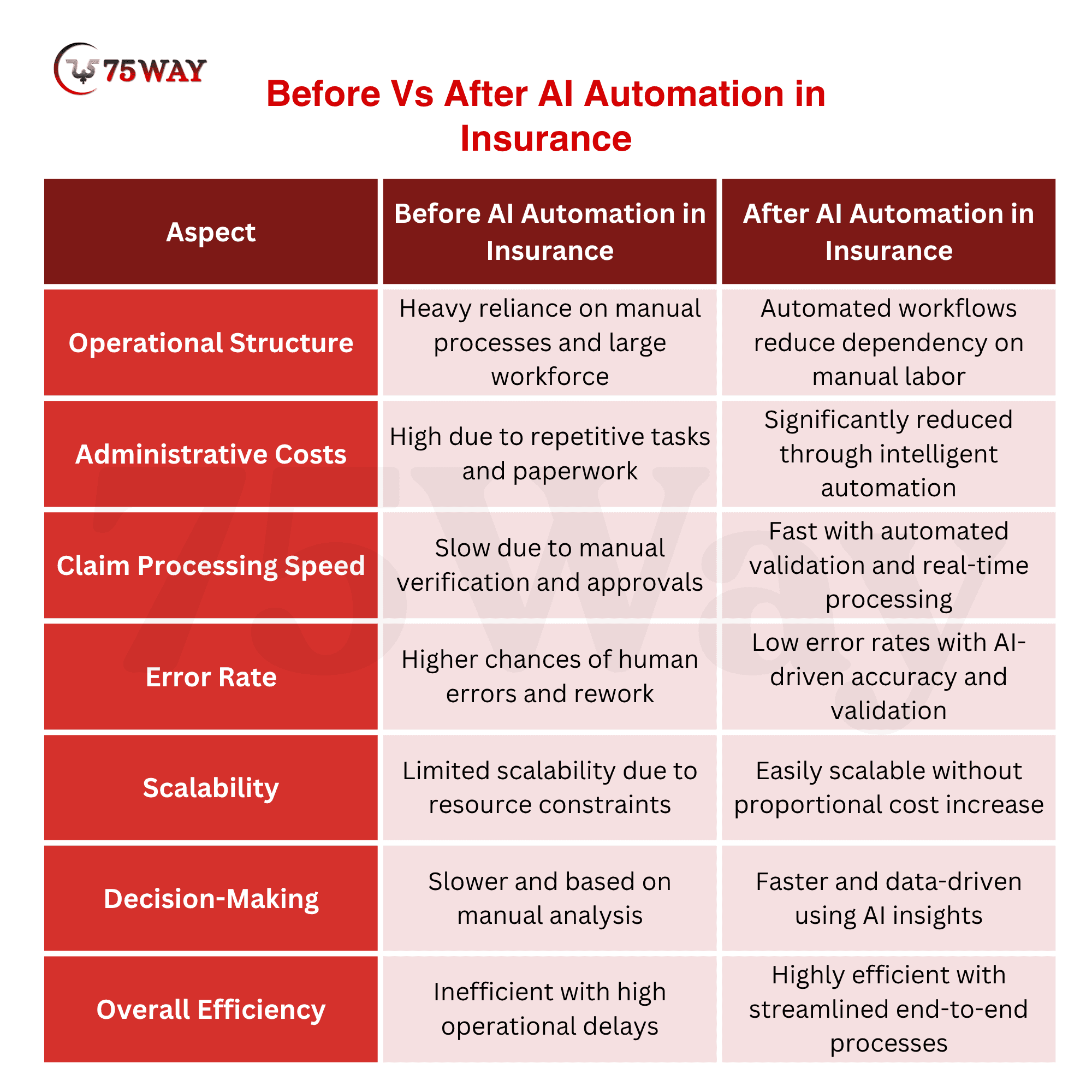

Insurance Operational Cost Transformation: Before Vs After AI Automation in Insurance

AI automation significantly changes the cost structure of insurance operations by replacing manual, time-consuming processes with intelligent workflows. Instead of relying on large teams for data entry, claims review, and policy management, insurers can automate these tasks to reduce operational waste and improve process consistency.

Before AI adoption, insurance companies faced high administrative expenses, slow claim cycles, and frequent human errors that increased rework costs. These inefficiencies directly impact profitability and limit the ability to scale operations efficiently.

After implementing AI automation, insurers streamline claims processing, underwriting, and customer service through data-driven systems. This leads to lower operational costs, faster decision-making, greater accuracy, and the ability to handle higher business volumes without proportional increases in costs.

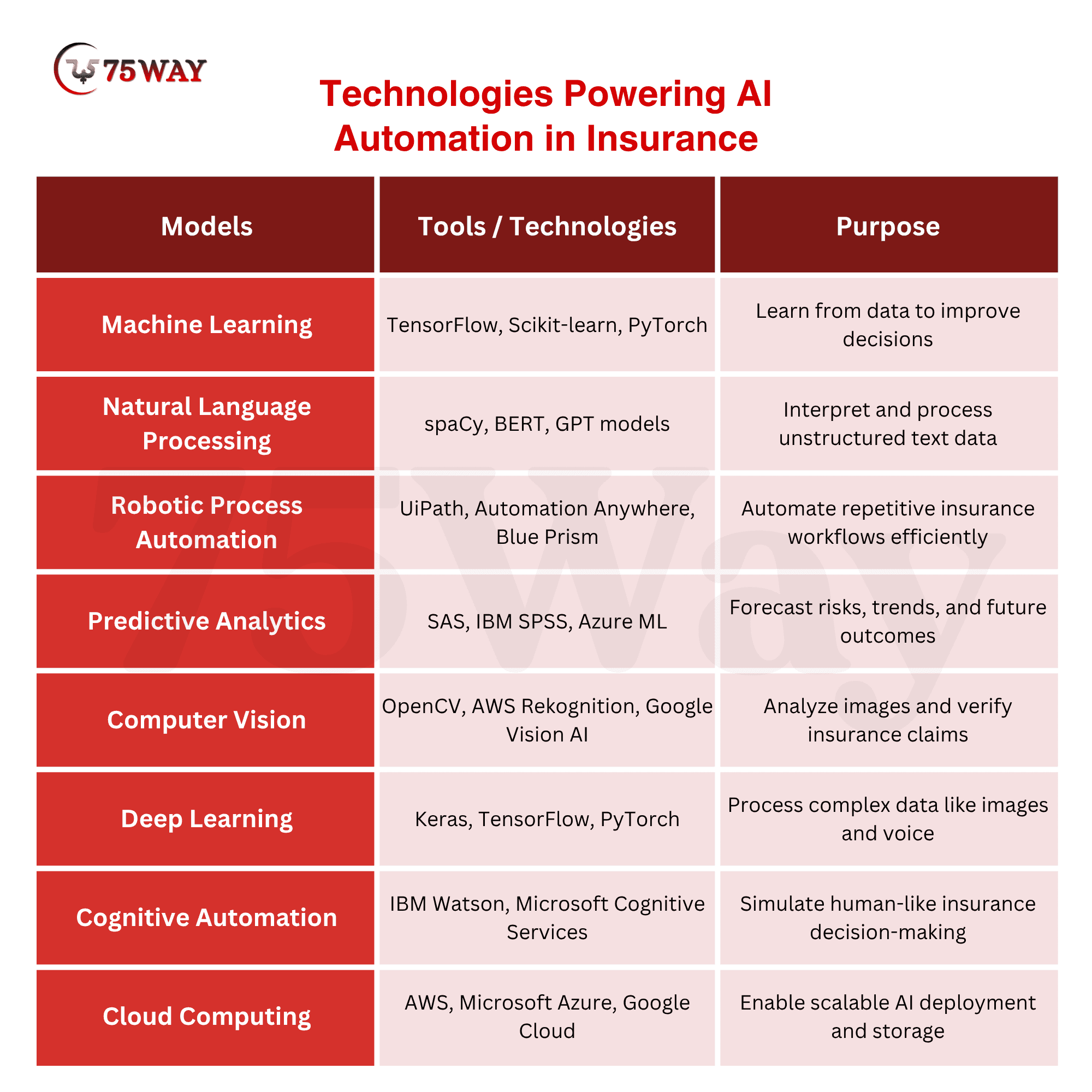

Technologies Powering AI Automation in Insurance

AI automation in insurance is built on a combination of advanced technologies that work together to replace manual processes, improve decision-making, and increase operational accuracy. These technologies don’t work in isolation—they integrate across underwriting, claims, fraud detection, and customer service to create a fully intelligent insurance ecosystem that is faster, more reliable, and cost-efficient.

- Machine Learning: Machine learning enables systems to learn from historical and real-time data to improve decision-making over time. In insurance, it helps in risk scoring, underwriting accuracy, and claims prediction. The more data it processes, the smarter and more precise it becomes.

- Natural Language Processing (NLP): NLP allows systems to understand and interpret human language from emails, documents, chat conversations, and claim descriptions. This is especially useful in customer support and claims intake, where large amounts of unstructured text need to be processed quickly and accurately.

- Robotic Process Automation (RPA): RPA automates repetitive rule-based tasks such as data entry, policy updates, and document transfers between systems. It reduces manual workload, eliminates delays, and ensures consistent execution of routine insurance operations without human intervention.

- Predictive Analytics: Predictive analytics uses statistical models and AI algorithms to forecast future outcomes such as claim likelihood, customer churn, or fraud risk. This helps insurers make proactive decisions instead of reacting after losses occur, improving profitability and risk control.

- Computer Vision: Computer vision analyzes images and scanned documents used in claims processing, such as accident photos or damage reports. It helps insurers verify claims faster, detect inconsistencies, and reduce dependency on manual inspection.

- Deep Learning: Deep learning enables AI systems to analyze highly complex datasets, such as voice inputs, images, and behavioral patterns. It is widely used in fraud detection and advanced risk modeling, where traditional methods fall short in accuracy.

- Cognitive Automation: Cognitive automation combines AI, machine learning, and reasoning capabilities to simulate human decision-making. In insurance, it supports complex workflows like claim adjudication by analyzing multiple data points simultaneously.

- Cloud Computing for AI Systems: Cloud platforms provide scalable infrastructure for running AI models and storing large volumes of insurance data. They enable real-time processing, remote accessibility, and cost-efficient deployment of AI-powered insurance solutions.

Final Thoughts

To summarize, AI automation is no longer a future investment for insurance organizations; it is a present-day competitive necessity. Companies that adopt intelligent automation across underwriting, claims, customer service, and fraud detection are achieving faster turnaround times, lower operational costs, and stronger profit margins.

The real advantage lies in combining data, technology, and strategy to create systems that continuously improve outcomes. As customer expectations rise and margins tighten, automation provides the efficiency needed to stay ahead. Insurance providers looking to reduce costs and build AI-powered insurance solutions can contact a reliable AI development agency.

Frequently Asked Questions (FAQs)

What Types of Insurance Tasks Benefit Most From AI Automation?

AI automation delivers the highest value in tasks involving large data processing and repetitive decision-making. Functions like fraud detection, customer onboarding, risk scoring, and policy recommendations benefit significantly because AI improves speed, reduces errors, and enables insurers to handle complex operations with greater consistency and efficiency.

How Does AI Improve Insurance Customer Experience?

AI enhances customer experience by providing faster responses, personalized policy suggestions, and 24/7 support through chatbots and virtual assistants. It reduces waiting time for claims and inquiries while ensuring consistent service quality. This creates smoother interactions and increases customer satisfaction, trust, and long-term retention rates.

Can Small Insurance Companies Use AI Automation?

Yes, small insurance companies can adopt AI automation through scalable cloud-based tools and pre-built AI solutions. They do not need large infrastructure investments. Starting with focused use cases like claims automation or chat support helps smaller firms improve efficiency, reduce costs, and compete effectively with larger players.

Is AI Automation Expensive For Insurance Companies To Implement?

Initial implementation costs vary based on complexity, but AI automation often reduces long-term operational expenses. Many solutions are available on subscription or cloud models, making them accessible. Over time, savings from reduced manual work, fewer errors, and faster processes typically outweigh initial investment costs.

What Challenges Do Companies Face With AI Adoption?

Common challenges include data quality issues, integration with legacy systems, lack of skilled professionals, and resistance to change. Companies may also face regulatory concerns. Overcoming these challenges requires proper planning, employee training, strong data governance, and gradual implementation of AI solutions across operations.

How Quickly Can Insurance Firms See ROI From AI?

ROI timelines vary depending on use cases and implementation scope, but many insurers begin seeing measurable benefits within months. Areas like claims automation and customer support deliver quick returns through cost reduction and efficiency gains, while larger transformations show stronger long-term financial impact over time.